What is Bitcoin?

Key takeaways

- Bitcoin is a digital currency that lets people send and receive payments directly, without needing a bank to sit in the middle of the transaction.

- It runs on a decentralised network, so no single company, government or reserve bank controls it, and every transaction is recorded on a public ledger called the blockchain.

- Australians can buy Bitcoin in fractions through a registered local exchange, making it easy to start with as little as you like.

A new type of money

Bitcoin is a cryptocurrency – a digital form of money that isn’t controlled by banks, governments, or any single organisation. Even BlackRock, the world’s largest asset manager, recognises Bitcoin as a legitimate global money alternative.

While traditional money is the coins or notes in your wallet, Bitcoin exists as code on a digital ledger called the blockchain. This ledger records every Bitcoin transaction permanently, and copies are stored across a global network of computers. Because it operates on this decentralised system, Bitcoin can be used worldwide.

The Bitcoin whitepaper explains how this all works.

A store of value

Bitcoin’s value comes from its built-in limited supply, which makes it scarce and in demand. Central banks can print traditional money in unlimited amounts while Bitcoin, on the other hand, has a fixed supply of just 21 million coins. That’s why many people use Bitcoin to preserve their wealth over time.

Explore Bitcoin halving to learn more about how Bitcoin’s fixed supply works.

Sculptures made out of thousands of Venezuelan Bolivar currency due to its limited value, source Tadey Travels

An investment

For 27.9% (7.5 million) of Aussies, Bitcoin and other crypto are also investments. Like any investment, there are risks and rewards. You can see average annual Bitcoin returns here, but it’s also important to remember that past performance doesn’t guarantee the results. Explore technical analysis and key crypto indicators to better understand this complex market.

A brief history of Bitcoin

Bitcoin was launched in 2009 by Satoshi Nakamoto, an anonymous person or group. Since then, Bitcoin has stood the test of time and remains the world’s most well-known and largest cryptocurrency.

First real-world Bitcoin purchase

On 22 May 2010, Laszlo Hanyecz made the first real–world transaction by purchasing two pizzas (worth about $38) in Jacksonville, Florida, for 10,000 Bitcoins. If he had held onto those 10,000 Bitcoins he’d be a billionaire as of November 2024 (roughly $1.5 billion dollars)! That’s some pretty expensive pizzas, at around $750 million a pop!

Bitcoin’s market growth

Bitcoin’s global market value (or market cap) has grown a lot over the years, increasing from just $1.5 million in 2010 to nearly $3 trillion as of 22 November 2024. As of November 2024, that total value is more than the market cap of Tesla or the entire GDP of countries like South Korea!

Alongside this upward climb in market cap, the price of an individual Bitcoin has also also hit some pretty incredible milestones. Starting from 2010, and the first Bitcoin transaction described above, the price of Bitcoin was around $0.0064. From there it has gone up, with some bumps along the way, from US$100 in 2013 to finally hit its long-awaited milestone of US$100,000 (roughly $155,341 Australian dollars) on Dec. 5 2024.

However, as exciting as all of this is, as you can see from the chart above, Bitcoin has highs and lows. Cryptocurrency is a volatile asset and can be subject to sharp declines over short timeframes.

How is Bitcoin created?

Bitcoin is created when new “blocks” of transactions are added to its blockchain, which requires the following steps:

- Building the block

Transactions are grouped together into blocks before being added to the blockchain. - Verification

Each block is verified by solving a complex cryptographic puzzle. Once solved, this puzzle acts like a key that locks (or encrypts) the block onto the blockchain. The block becomes incorruptible at this point, helping the network stay secure. - Mining

Solving the puzzle linked to a block requires a lot of computing power, which miners provide. Miners use powerful, specialised computers to solve these block puzzles. The first to crack the code gets to add the block to the blockchain. As a reward, miners earn newly created Bitcoin and transaction fees. - Bitcoin supply

Once mined, Bitcoin can be sold into the market, gradually increasing the total supply.

What is the Bitcoin price now?

For live Bitcoin prices, sign in to your free bitcoin.com.au account via our mobile app or your browser. From there, navigate to the “Coins” tab to see current price movements on our interactive market tracker. You’ll find real-time price movements and insights across a range of cryptocurrencies, not just Bitcoin.

Platforms like bitcoin.com.au make it easy to buy, sell, and store Bitcoin securely in Australia.

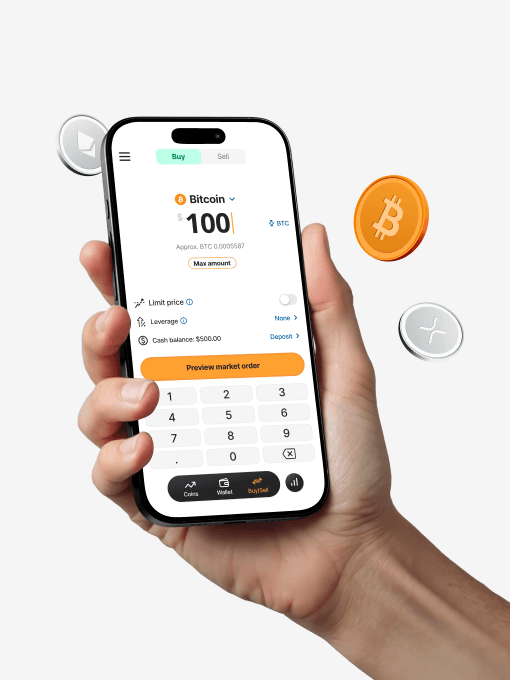

How to buy Bitcoin in Australia

Bitcoin.com.au has been helping Australians buy Bitcoin since 2013. Trusted by 500,000+ Australians and serious about security.

You can buy Bitcoin in minutes. Start with as little as you like, no need to buy a whole coin.